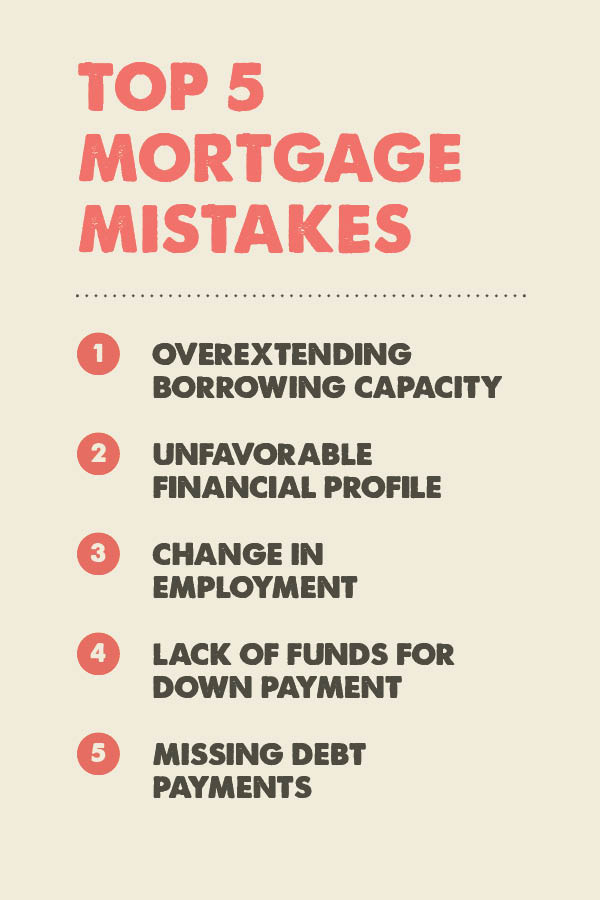

Five ways to hinder home loan approval and how to avoid them

Although mortgage qualification varies by lender and loan type, all homebuyers can improve their odds of securing loan approval by avoiding actions and decisions that may call their financial management into question.

Farm Credit Services of America (FCSAmerica), a portfolio lender that specializes in financing homes in the country and rural communities, developed the following list to help your clients understand the factors that can harm their creditworthiness and how to avoid them.

1. Overextending borrowing capacity

Calculating affordability requires homebuyers to be realistic about their borrowing capacity. Stretching borrowing limits can quickly create financial stress. As a general rule of thumb, homebuyers should plan to purchase a property that’s worth no more than three times their total gross annual income, and if estimating a monthly mortgage payment, remember to factor taxes and insurance.

Because debt-to-income ratios demonstrate a homebuyer’s ability to handle monthly payments and repay debt, homebuyers should avoid taking on new debt while their application is under review and put off major purchases until after loan closing.

2. Unfavorable financial profile

When applying for a home loan, homebuyers should expect to share their full financial profile, including their debt and credit history.

Failing to report debt challenges the accuracy of the financial documentation homebuyers submit in their loan application and may cast doubt on the applicant’s character. Homebuyers should always disclose debt up front and respond quickly if asked to provide additional financial information.

Similarly, lenders use credit scores to assess risk and make objective predictions about future financial behavior, but homebuyers don’t necessarily need a traditional credit profile to prove their loan eligibility. Depending on the lender and loan program, homebuyers may be able to boost their credibility as a borrower by reporting other on-time payments such as rent or utility bills.

3. Change in employment

Employment history establishes whether a homebuyer has a predictable source of income to support their mortgage payments. If a new career opportunity is on the horizon, homebuyers should be prepared to verify any change in employment income to avoid loan processing delays.

For those who farm or are self-employed, verifying income may require additional steps. In order for a second job to count towards overall income, the job must have been held for at least two years.

In general, lenders will want to review a homebuyer’s past two years’ personal and business tax returns, their most recent paystub and an updated balance sheet.

4. Lack of funds for down payment

Homebuyers who dismiss their down payment run the risk of not having cash available when they’re ready to buy. Setting aside down payment funds early on in the home loan application process will bring peace of mind to both the borrower and their lender.

Underestimating the costs of buying and furnishing a home can also leave homebuyers feeling strapped for cash. In the months prior to house hunting, it’s good practice for homebuyers to cut unnecessary spending and save three to six months of living expenses as an emergency cash reserve.

5. Missing debt payments

Finally, missing a payment during the loan application process may interfere with mortgage approval. Homebuyers who keep careful records and pay their debts early can be reassured their accounts are properly credited and their mortgage application is current.

Homebuyers who have a history of missing debt payments are also likely to raise credit concerns. While recovering from negative credit takes time, it’s important for homebuyers to monitor their spending and immediately begin resolving any patterns of financial mismanagement.

Don’t let these mishaps prevent your clients from financing their country dream home. Lenders like FCSAmerica are here and ready to help.

Click here for more information about rural home and acreage mortgages.